An auditor most likely would limit substantive tests of sales transactions when control risk is assessed as low for the existence or occurrence assertions concerning sales transactions and the auditor has already gathered evidence supporting. And retained earnings comes from the earnings or losses on the income statement.

Audit Expenses Assertions Risks And Procedures Wikiaccounting

Board of Trustees of.

. As auditors we usually audit inventory by testing the various audit assertions including existence completeness rights and obligations and valuation. Inspecting payroll tax returns. The assertions applicable to Cash Disbursements are.

In this section we will cover various substantive audit procedures for inventory for each types of assertions that we mentioned in the above section. Other bodies added on 1st April 2015. Investments in the Balance Sheet.

Audit assertions for investments. The assertions listed in ISA 315 Revised 2019 are as follows. When the office supplies are utilized during the month an audit adjustment entry will be made to credit prepaid office.

Accounts payable balances reported on the balance sheet include all payable transactions that have occurred during the accounting period. Cash purchases have happened when an entity makes a purchase of goods or renders the services and then makes the payments by cash immediately. Investments are audited by testing various audit assertions as existence completeness valuation and rights and obligations.

In the audit of investments we test the valuation assertion to ensure that the investment. Sales purchases and account balances eg. B cash receipts and accounts receivable.

Audit procedures to Ensure Completeness. The audit is an art of systematic and independent review and investigation on a certain subject matter including financial statements management accounts management reports accounting records operational reports revenues reports expenses reports etc. The audit assertions for fixed assets are included in the table below.

1 The auditors consideration of illegal acts and responsibility for detecting misstatements resulting from illegal acts is defined in AS 2405 Illegal Acts by ClientsFor those illegal acts that are defined in that section as having a direct and material effect on the determination of financial statement. The audit risk for Cash Disbursements is generally low but it also heavily depends on how well the entitys internal control policy is. Inspecting investment securities on hand and comparing with previous year balances and accounts along with purchases and sales in the current.

An integration joint board established by order. What are Substantive Procedures. Footnotes AS 2401 - Consideration of Fraud in a Financial Statement Audit.

The following are the accounting records for both purchases on credit and cash purchases. The result of reviewing and investigation will be reported to shareholders and other key internal stakeholders. Auditors have limited time to conduct the audit and they need to submit An audit report is a document prepared by an external auditor at the end of the auditing process that consolidates all of his findings and observations about a companys financial statements.

Vouch new purchases and disposals of investments to supporting documents eg. Put the relevant assertions next to each audit stepthis makes the connections between the RMMs at the assertion level and the audit steps clear. When control risk is assessed as low for assertions related to payroll substantive tests of payroll balances most likely would be limited to applying substantive analytical procedures and A.

Audit assertions for accounts payable. Confirms sales values and purchases costs ie. Accounts Commission for Scotland.

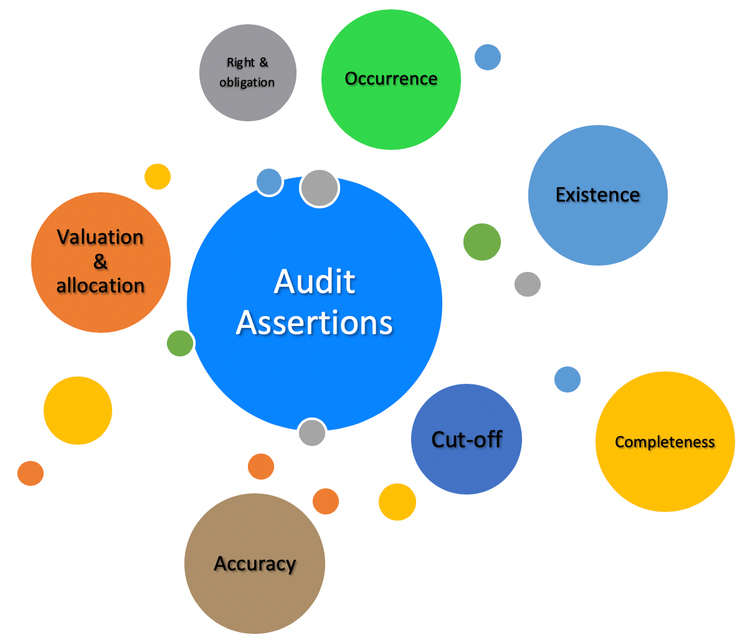

Assertions about classes of transactions and events and related disclosures for the period under audit i Occurrence the transactions and events that have been recorded or disclosed have occurred and such transactions and events pertain to the entity. Second many forms of theft occur in the accounts payable area. Usually the control procedures of.

This could be the result of intentional fraud or. Thus in this section we will take some assertions that we usually test in. Most of the business prefer to make the payments by banks transactions to minimize the fraud case.

Whilst the procedures are perhaps similar in nature their purpose and relevance is to test different assertions regarding inventory balances. The balance sheet contains many items including assets owned by the business liabilities to be paid by the business and equity in the financing structures. Accounts payable is usually one of the more important audit areas.

Footing and crossfooting the payroll register. This test can be performed by selecting purchases and sales of the items for the few days before and after the end of the accounting period to ensure that transactions related to items are recorded in the correct accounting period. Observing the distribution of paychecks.

These are explained in detail below. By inspecting the invoice. Key Audit Procedures for Inventory Audit.

See page 64 and Chapter 16 of the notes assertions relate to classes of transactions eg. The presentation of all these items on a single page help to understand the financial position of the business. Audit assertions for fixed assets.

To ensure the completeness of inventories we shall need to perform the below procedures. For an auditor to be reasonably assured of the Cash Disbursements made by the entity tests will be performed to cover the audit assertions. First its easy to increase net income by not recording period-end payables.

And should I perform fraud-related expense procedures. In this post Ill answer questions such as how should we test accounts payable. A opening and closing inventory balances.

Read more the audit report The Audit Report An audit report is a document. Substantive procedures are the method or audit tests designed by an auditor to evaluate the financial statements of the company which require an auditor to create conclusive evidence for verifying the completeness accuracy existence occurrence measurement and valuation audit assertions of the financial records of the business. The internal controls for account payable are directly linked to the clients internal controls of the purchases.

With our money back guarantee our customers have the right to request and get a refund at any stage of their order in case something goes wrong. Generally speaking the balance sheet is an equation where assets equal. Audit Evidence This section explains what constitutes audit evidence in an audit of financial statements and addresses the auditors responsibility to design and perform audit procedures to obtain sufficient appropriate audit evidence to be able to draw reasonable conclusions on which to base the auditors opinion.

Investments reported on the financial statements really exists at the reporting date. In order to audit the accounts payable it requires to use the combination of analytical procedures and tests of detail or substantive audit procedures for accounts payable. If we disregard stock purchases and sales equity is usually the accumulation of retained earnings.

Collectively all classes of transactions account balances and their related disclosures make up the financial statements. Typically we perform the audit of accounts payable in conjunction with the audit of purchases. Prepaid expenses are known as assets that are being paid for and then used gradually during the accounting period ie office suppliesA company purchases and pays for office supplies and as they are consumed they will become an expense.

The National Convener of Childrens Hearings Scotland. One high risk of inventory is that the company bought the inventory but the purchases were not recorded into the inventory account. Other bodies and offices added on 5th March 2012.

Audit assertions for Investments.

Understanding Audit Assertions A Small Business Guide

Audit Procedures Types Assertions Accountinguide

Inventory Audit Assertions Substantive Tests Youtube

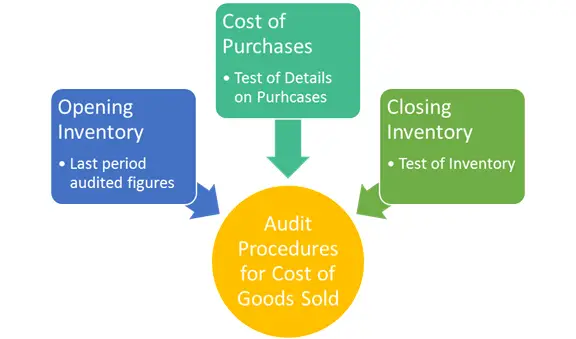

Auditing Cost Of Goods Sold Risks Assertions And Procedures Audithow

0 Comments